The hardest part of investing is making judgement calls in real time, especially at inflection points. How do you decide if this is a new bull market or just a nasty bear market rally? Ultimately, we really won't know until its too late and already obvious. In hindsight all market calls are easy. However, in real time that is what separates the good investors from average. Successfully trading the markets is not about certainty. It is about putting the odds in your favor and exploiting the edge you have. We make bets on probabilities and then let price action be the final determinant. Below we'll lay out the data and hope that helps shape a thesis. Lets get to it.

One of the better gauges of sentiment we study is the monthly BofA fund manager survey. It provides a good read into the positioning and sentiment of fund managers around the globe. Below are the key takeaways from the most recent survey.

BofA February Global Fund Manager Survey

Bottom line: "pain trade" still up according to Feb FMS; investors least pessimistic since Feb'22 but nowhere near optimistic enough to say positioning a sell catalyst; cash as % AUM still >5% & FMS BofA Bull & Bear Indicator up just a tad from 4.4 to 4.5.

The Big Numbers: 68% say China reopen is inflationary, 66% say US$ to fall, 66% say it's a bear rally, 65% say yield curve to steepen, 64% no Russia-Ukraine truce this year.

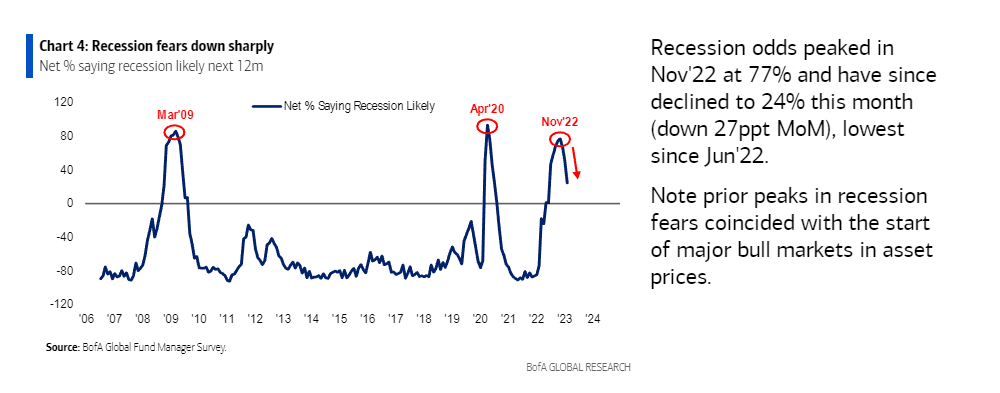

On Macro: last Nov net 77% predicted recession…in Feb just 24% do; global growth expectations now least pessimistic in a year (net 35% expect weaker economy); biggest "tail risk" still "higher-for-longer" inflation (i.e. monthly core CPI readings of >0.4%).

On Policy: dovish optimism on Inflation & Fed rising…most investors since Mar'20 see rate cuts next 12 months, most since Sep'21 expect steeper yield curve.

On Risk: cash levels down to 5.2% from 5.3%; most "crowded trade" no longer "long US$," replaced by "long China stocks" & "long IG bonds."

On AA: investors OW cash (42%), OW commodities (15%), UW equities (-31%); record 3-month jump in exposure to EM stocks (Chart); short-covering tech/consumer stocks, more length in bank stocks, investors UW defensives vs cyclicals 1st time since Apr'22.

Contrarian trades: long stocks, US, tech and short cash, China, banks.

Fund managers remain pessimistic even after a strong rally to start the year.

Cash allocations remains elevated with plenty of dry powder to be put to work.

Recession fears have declined and one reason why the markets have rallied off the lows.

Now we know why investors remain cautious. Most believe this is a bear market rally rather than a new bull market.

Long cash and emerging markets and bearish on US equities and real estate.

Below is a tweet from Ryan Detrick showing some bullish precedent based on research from Ned Davis.

On top of that the market breadth has been impressive on the upside. In fact, on January 12th we had two massive bullish momentum breadth signals fire off. The Deemer BAM and the Whaley breadth thrust. Below is a nice recap from Quantifiable Edges shows the multiple breadth thrust signals and the forward returns associated with them.

If this is a bear market rally, the current move is par for the course. If we remain in an extended bear we could have further to go on the downside. This tweet from Charlie Bilello compares the rallies to the 2 other nasty bears in 2007-2009 and 2000-2002.

If inflation remains elevated longer but we don't slide into a bigger recession maybe the worst is behind us for the markets. But also we could be dealt with a frustrating sideways market. This analog from Jurrien Timmer from Fidelity makes that case.

If the current rally persists, traders will be pricing in the possibility of soft landing and a Goldilocks economy. That would look like inflation pulling back but the economy avoiding a recession. If that happens the market should be slightly overvalued here. If not, we may be at the end of the range from a valuation perspective. Research from 3Fourteen Research sums this up nicely.

Based on the evidence above, most traders remain cautious and underweight equities with plenty of cash on the sidelines. They are positioned for a bear market rally rather than a new bull market. If this is a new bull, they will be forced to chase price higher which in turn could drive the market even further as cash from the sidelines piles in. The markets remain elevated with regards to valuation, but if the breadth thrust signals a new bull market, the valuation will remain higher for longer. The contrarian trade is to stay long US stocks until sentiment gets overheated. Markets seem far from there as of now as it continues to climb the wall of worry.