Friday marked the final trading day of the month and its 2.5% surge was easily the biggest up-day of the month and the best day for the market since September. Since the January 20th "bottom" the S&P has added nearly 4.5% with oil/energy related stocks seeing the largest oversold bounces. Chart below from Bespoke.

At mid-month, the S&P had just posted the worst 10-day start to a year in history and quickly dove under last August's lows and ultimately traded at levels not seen since October 2014.

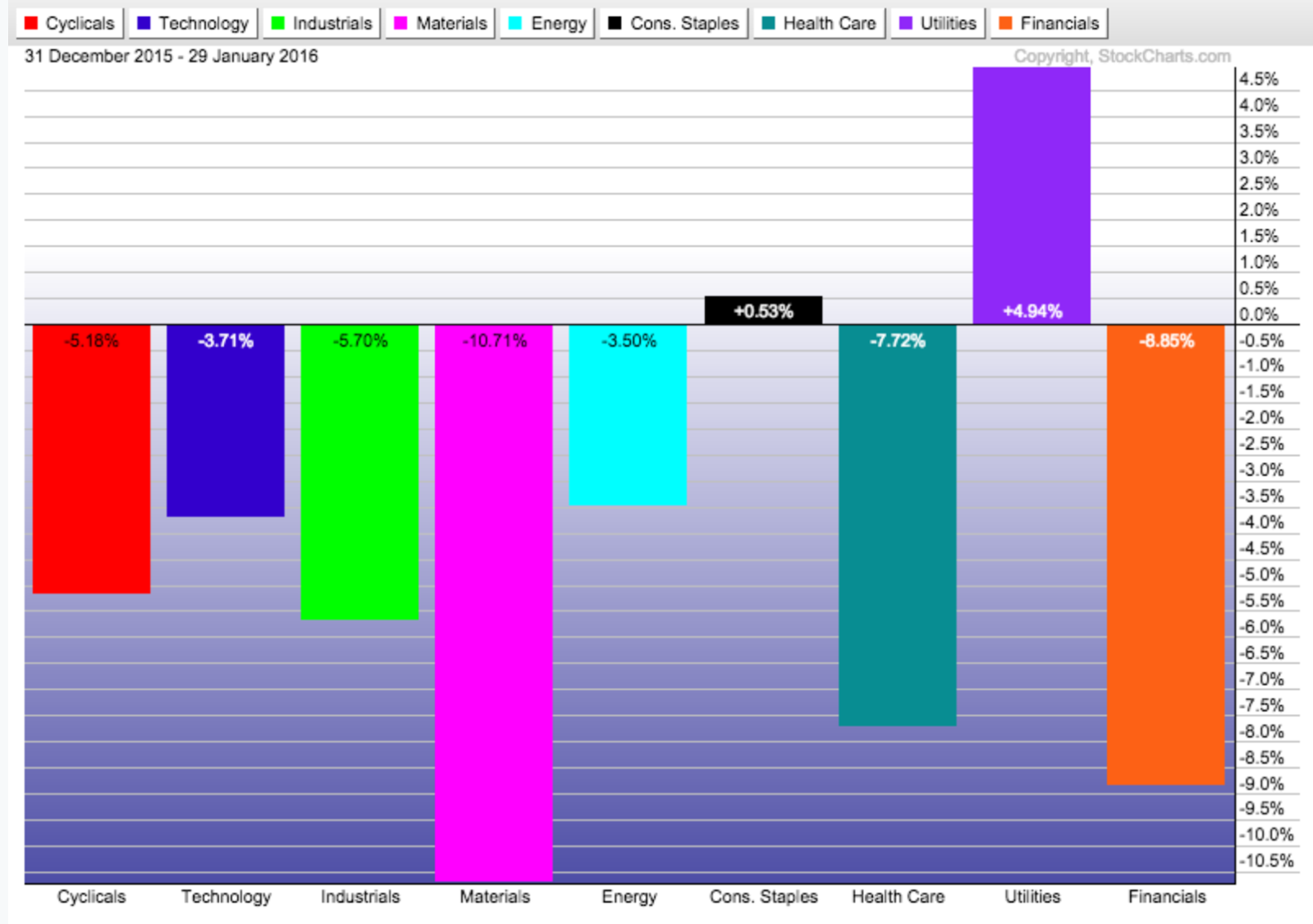

The cause? Well, it looks like a combination of oil's plunge (crude broke below $30/barrel), the slowing Chinese economy and our market signaling to the Federal Reserve that it may want to reconsider any additional rate hikes here in the near-term. Those headline factors and a continued narrowing of leadership and breadth were enough for sentiment to spoil and left investors seeking the comfort of cash. Earlier in the week we noted that some rotation was occurring as defensive sectors like Utilities and Staples were being favored. In fact, they're the only two sectors in the S&P with positive year-to-date performance.

For now, it looks as if the market is enjoying a relief rally that was well earned. In fact, we noted last week that on one of our measures the market had reached historically oversold levels. When the S&P was visiting the low 1,800s on January 20th, the percentage of stocks trading above their 200-day moving average had fallen to an incredibly low 11.48%. This was a number comparable to some of the readings seen during the most severe corrections over the last 20 years. However, we also made sure to note that the market did not typically register its price lows at the same time. We cautioned that momentum typically bottoms before price and what we'll often see is price requiring another re-test of the lows (creating positive divergence) before turning higher.

On to February...