The monthly BofA global fund manager survey is a good way to keep a pulse on the sentiment of fund managers. Below are the key takeaways from the most recent survey.

BofA August Global Fund Manager Survey

Bottom line: least bearish FMS since Feb'22; cash drops from 5.3% to 4.8% (21-month low), 3 out of 4 expect soft/no landing, smallest equity UW since Apr'22, largest tech OW since Dec'21; bear positioning strong tailwind for risk assets in H1…not the case in H2.

On Macro & Policy: global growth expectations up to net -45%, 4/10 say recession "unlikely" (was 1/10 Nov'22), EPS optimism highest since Feb'22; US fiscal policy as stimulative today as at Covid peak (Dec'21) yet expectations for lower rates now highest since Nov'08.

On Risks: FMS cash <5% means end of BofA Global FMS Cash Rule contrarian "buy signal"; biggest "tail risk" still inflation keeps central banks hawkish; most likely "credit event" is US/EU CRE at 45% (note China real estate relatively low at 15%).

On Asset Allocation: out of cash & REITs (capitulation to GFC/Lehman levels - Chart 1) into stocks & commodities; out of US/EU/UK into EM/Japan; out of industrials/utilities into energy/tech (long Big Tech by far most "crowded trade").

Contrarian trades: for risk-on (SPX to 4.8k) top trade is "long REITs, short bonds"; for risk-off (SPX to 4.2k…our view) "long utilities, short tech"; REITs most fascinating to watch: if no recession, FMS says go max long, but if REITs can't recover with Lehman-like positioning, then recession could be just around the corner.

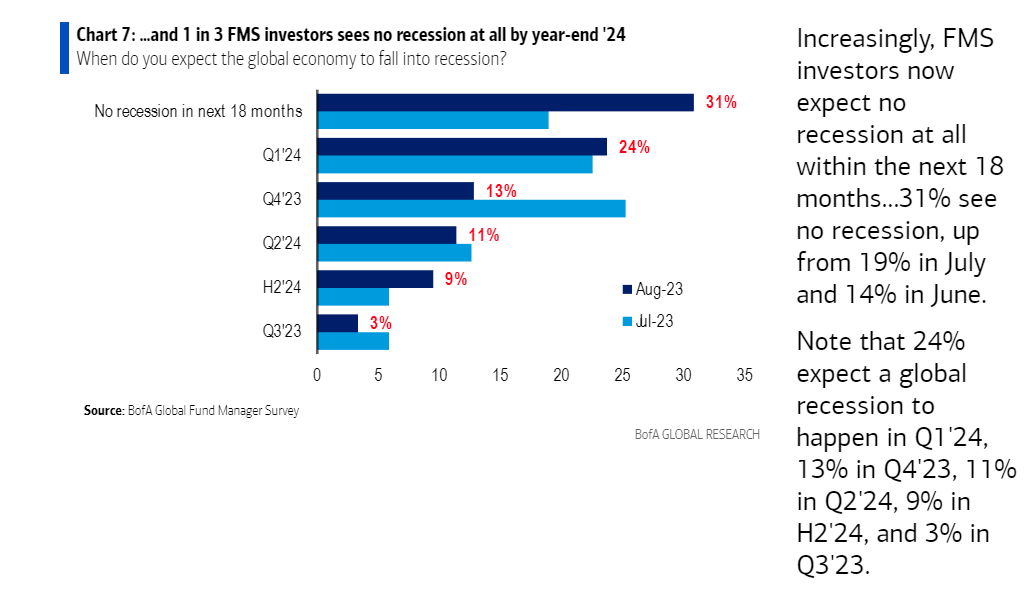

Below are some of the more interesting charts about sentiment and expectations:

FMS sentiment improving and now the least bearish since Feb '22.

Consensus remains for a soft landing.

Expectations for lower bonds yields are hovering around 20-year highs.

Lower bond yields contradicts the expectations that the Fed will lift its inflation target.

Inflation still remains the biggest worry of fund managers.

While the most crowded trade remains long big tech by a wide margin.

Cash is being put to work into equities, EM, Japan, tech, and energy.

A tweet from Jay Kaeppel shows why inflation is so important to stock market returns.

One area to watch is seasonality as we enter a potential choppy period during the back half of a pre-election year.

Based on the data presented, fund managers have clearly turned more bullish as they have crowded into big cap tech stocks. Inflation remains the biggest worry even as recession fears have waned. Yet, the seasonal pattern favor a choppy sideways range with a strong finish. Based on the strong start to the year, a pause would be welcomed before we resume higher. Only time will tell.