After a banner year last year for growth and momentum, 2021 has been a historically frustrating year. With the S&P up double digits again YTD it is surprising that certain sectors are drastically underperforming. So what do you when your strategy is out of favor while the general market doesn't show any signs of weakness? If you invest long enough all investors and managers will go through difficult periods. The key is to know your strategy in and out and know when it is time to be aggressive and when it is time to be more risk adverse and selective. If we take a quick look at some data and statistics we can get a better idea of what is being rewarding in this environment.

Lets take a top down approach and look at which asset class is leading. We can see that commodities are in the lead as bonds lag drastically.

Commodities have been on fire.

If you want a reason for why commodities are surging we can look at the recent March PPI prices:

- Plywood (construction): +53 percent vs. last year

- Cold rolled steel (durable goods): +75 pct

- Copper (construction, durable goods): +43 pct

- Corn (food, animal feed): +44 pct

- Wheat (food): +32 pct

One of the big surprises of the first quarter was the historic rise in interest rates. The 10-year treasury note started the year around 90 basis points roughly doubling to 175 basis points. Albeit from a very low starting point, the 10-year yield put in the biggest 40-week rise in rates, by a long shot, going back 50 years. Below shows how dramatic the rise in yields has been YTD across duration's.

The increase in yields put the biggest pressure on high valuation growth stocks. Many growth stocks are in bear market territory even with the general market positive on the year. This bifurcation is the exact opposite of what worked last year. Toni Sacconaghi, a longtime technology analyst at Bernstein, encapsulated the dynamic in a fascinating piece of research. “He points out that, in 2020, investors seemed to be buying techs almost because of their high price tags. In fact, if you divide the tech universe into quintiles ranked by price/earnings ratios, the returns were lowest for stocks with the lowest valuations—and highest for those trading at the loftiest multiples. The average tech issue outpaced the broad market by 28 percentage points last year, but those in the top quintile outperformed by 60 percentage points. Writes Sacconaghi: The more expensive a stock was in 2020, the better it generally fared. But investor behavior is shifting. Tech shares have underperformed the broad market by about four percentage points this year, according to Sacconaghi. The most expensive names are running 10 points behind and the stocks at the other end of the valuation spectrum—the cheapies—have beaten the market by about 6%. In short, what went up is indeed starting to come down, he writes.”

The correction in high quality growth names will set up future

opportunities, as YTD is a tale of two tapes and the opposite of last

year. There was a huge rotation out of growth and into value, small

caps, and the reopening theme. Below is a good representation of the

shift out of growth and into value. It is a ratio chart of the VUG

(Vanguard Growth ETF) to the VTV (Vanguard Value ETF). When it is

rising, growth is outperforming which we see with the historic rise last

year. This trend started to stall out in the fourth quarter of last

year and broke down in the first quarter of this year as money rotated

away from high growth and into more value centric ideas. It now has the look of a big head and shoulders top with a retest failure.

When we drill down to market capitalization we can clearly see smaller caps are outpacing large caps.

Lastly is a list of sector returns year to date. When beaten down energy and financials are leading the market that is not a ripe environment for growth. The current market clearly favors cyclicals and commodities.

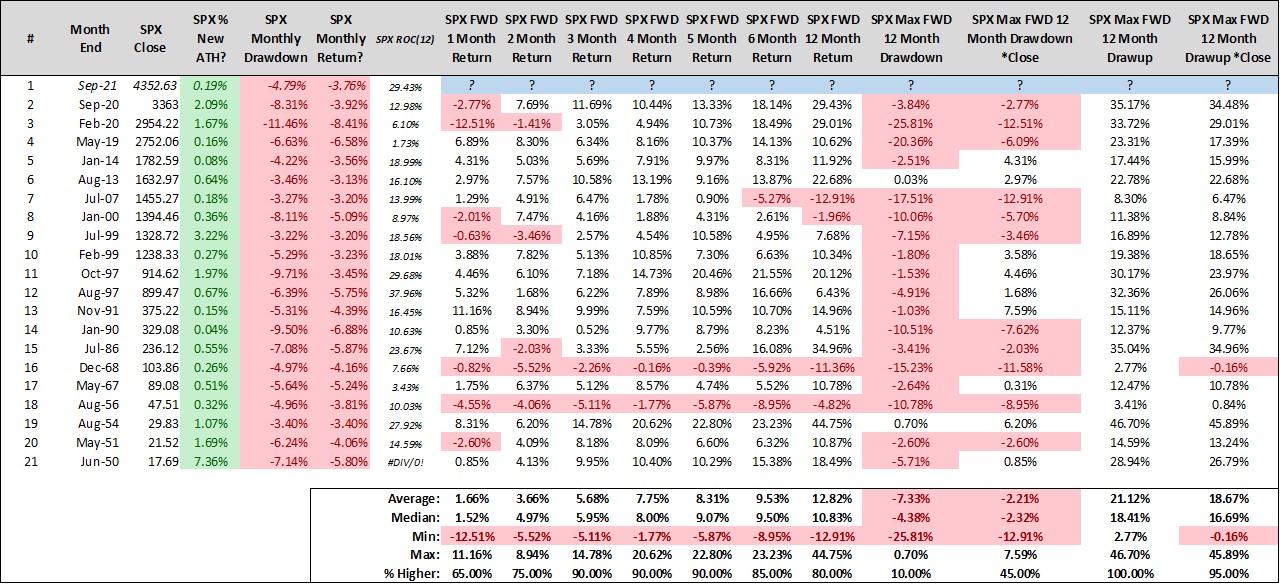

Now that we have an idea what is working and what isn't we can look at a few data points that gives some future potential. A few studies from Ryan Detrick show conflicting possibilities. Even though we are entering the worst 6-month stretch of the year, based on some recent data the future looks brighter.

A second tweet from

Ryan Detrick shows how this current bull trend could be getting close to exhausting itself in the short term.

As we enter the sell in May and go away theme for the next six months, one data point helps back up this case. A recent note from DataTrek research shows "the latest Investment Company Institute money flow data for long

term mutual/exchange traded fund flows paints a less optimistic picture. We now

have data through April 28th (essentially month end); here’s how it looks:

- Fund investors redeemed $17.8 bn from US equity funds

in the final week of April, enough to flip whole-month flows negative to

the tune of -$7.8 bn.

- There were also $4.6 billion in non-US equity fund

redemptions, but April’s total is still positive by $17.6 bn.

- Fixed income fund flows, by contrast, were strong last

week (+$19.2 bn) and April as a whole looks like inflows will total $76.2

bn. That’s the best month for this asset class since January’s $93.8 bn of

inflows.

- Commodity fund (mostly physical gold) inflows last week

were slightly positive (+$119 mn) but April’s outflows still total $1 bn.

Takeaway: it’s just one week of data, but the sudden and sizable

reversal in US equity fund flows after 2 solid months of inflows isn’t

something we can just dismiss, especially given the money market fund data. Perhaps

investors are starting to sell positions with large capital gains (those would

more commonly be in US vs. non-US equities) now that the current

Administration’s tax plan is out. Perhaps stimulus money going into US equity

funds has run its course. Perhaps late April’s sales were just rebalancing.

Perhaps it’s all of the above. One thing is for sure: it will be much easier

for US equities to continue their rally if flows turn positive again. We’ll

know soon enough."The question is what do we do when our strategy is out of favor. I have been in the business long enough to know that styles ebb and flow with market cycles. Not one strategy dominates every market year in and year out. Where most amateur investors fail is they get complacent and chase the next hottest investment product. However, if you know your methodology and trust the process you have confidence that opportunities will eventually present themselves. Sometimes the best trade is to do nothing while the hardest trade is to keep powder dry while reducing risk sitting patiently for asymmetrical bets to turn up.

A quote from Dr. Brett Steenbarger sums up how a trader should react under uncertainty, "that is where meditation and self-control techniques learned through

biofeedback can be very helpful. If market volatility has picked up,

there will be plenty of movement to participate in. The key is standing

back, slowing yourself down, consulting the data and then looking for

opportunity. Because the volume and volatility are coming from large

participants in the marketplace, their behavior can create significant

directional opportunity. You just want to be at your mindful best at

those times so that you size positions properly and don’t let the

excitement lead to overtrading. A lot of money can be lost quickly under

chaotic conditions."

{kind=link}