BofAML March Global Fund Manager Survey

"Pain trade" for stocks is still up: in the BofAML March Global Fund Manager Survey (FMS), profit expectations rose, rate expectations fell, and cash levels fell from 4.8% to 4.6%; yet allocations to stocks dropped to their lowest level since Sep '16; there is simply no "greed" to sell in equities.

Growth & EPS expectations rose for 2nd consecutive month: but China & corporate debt concerns linger: the biggest "tail risk" for investors is a "China slowdown" (not "trade war");asked what companies should do with cash flow, 46% of respondents said "improve balance sheet", 29% said "increase capex" (lowest since Oct'09), 18% said "increase buybacks".

Interest rate expectations fell: more than 1/3 believe the Fed hiking cycle is over, 53% say short-term rates will be unchanged or lower over the next 12 months, and FMS bond yield forecasts are now the lowest since Jul'12, a big reason cyclical stocks remain shunned.

Asset allocations look pessimistic: investors are long defensive assets that perform well when growth & rates fall, and short cyclical assets that perform well when growth & rates rise (Chart 1); allocation to bank stocks dropped to the lowest since Sep '16.

Crowds & contrarians: the most crowded FMS trade is short European stocks; overvaluation of US$ is the highest since Jun '02; relative to 20-year FMS history investors long cash;"long stocks-short cash", "long EU-short EM", "long industrials-short REITs" are all contrarian.

Rules & tools: BofAML Bull & Bear Indicator stays at a neutral 4.7; FMS cash rule & FMS volatility rule say "long risk"; FMS relative value models more defensive.

After

a 20% move off the December lows in the S&P 500, fund manager still

find themselves underwhelmed and under exposed. There remains no

euphoric greed even after such a strong move. This bodes well for the

bulls and the pain trade continues to haunt the bears. Fund managers

favor defensive names and cash even as their expectations for growth and

profit improve.

While 38% of fund managers say they think the Fed is done hiking rates and the fed funds futures markets are pricing in 13bp of Fed rate cuts in the next 12 months. This still doesn't make managers bullish as equities cannot catch a bid with global equity allocation the lowest since September of 2016. Global equity allocation stands at just 3% overweight and has only been negative once in the past 6 years.

While 38% of fund managers say they think the Fed is done hiking rates and the fed funds futures markets are pricing in 13bp of Fed rate cuts in the next 12 months. This still doesn't make managers bullish as equities cannot catch a bid with global equity allocation the lowest since September of 2016. Global equity allocation stands at just 3% overweight and has only been negative once in the past 6 years.

A slowing China economy

takes the top spot as the biggest tail risk, followed by a trade war and

corporate credit crunch. These worries seem to be weighing on investors appetite for risk as only 30% of fund managers are net long equity markets, which is the lowest since December 2016 and a massive reversal from 55% net long in September 2018.

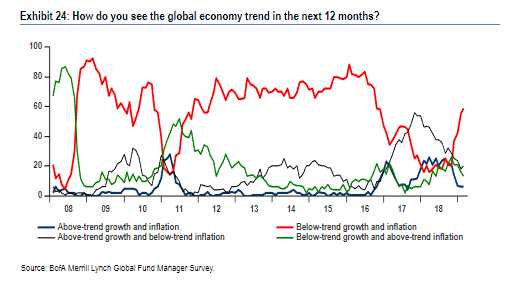

It is easy to understand

why fund managers are pessimistic. 59% of

FMS investors are bearish on both the growth and inflation outlook for the

global economy over the next 12 months, the highest since Oct'16, cementing the

return of secular stagnation as the consensus view amongst FMS

investors. This also explains why investors are only 3% overweight global

equity allocation. This is the lowest since Sept '16, a

massive drop from 31% overweight as recently as Nov '18 as investors turn

skittish on equities despite global stocks +12% YTD. FMS equity

allocation has only been negative once (Jul '16) since 2012.

Since the market top in October there has been a battle between bulls and bears and the recent survey underscores the gloomy outlook for the

bears. There is a divergence between

sentiment and price which should break the market in a clear direction. Will the bears win, and the trend turn lower on

the back of slower growth and over-valued dollar? Or is there something under the surface that has

propelled this market higher in a ferocious rally straight off the bottom. A case can be made if the bears throw in the towel and increase their allocation to equities, the pain train will endure. We remain in the bullish camp as the price

appreciation should continue with further gains. However, that doesn’t mean there won’t be downside

volatility and choppy frustrating trading ranges. We just don’t believe the markets are ready

to implode as the bears predict and hope. The sentiment data favors the bulls and leaves plenty of room for the upside and euphoria and greed to set in as the rally continues.