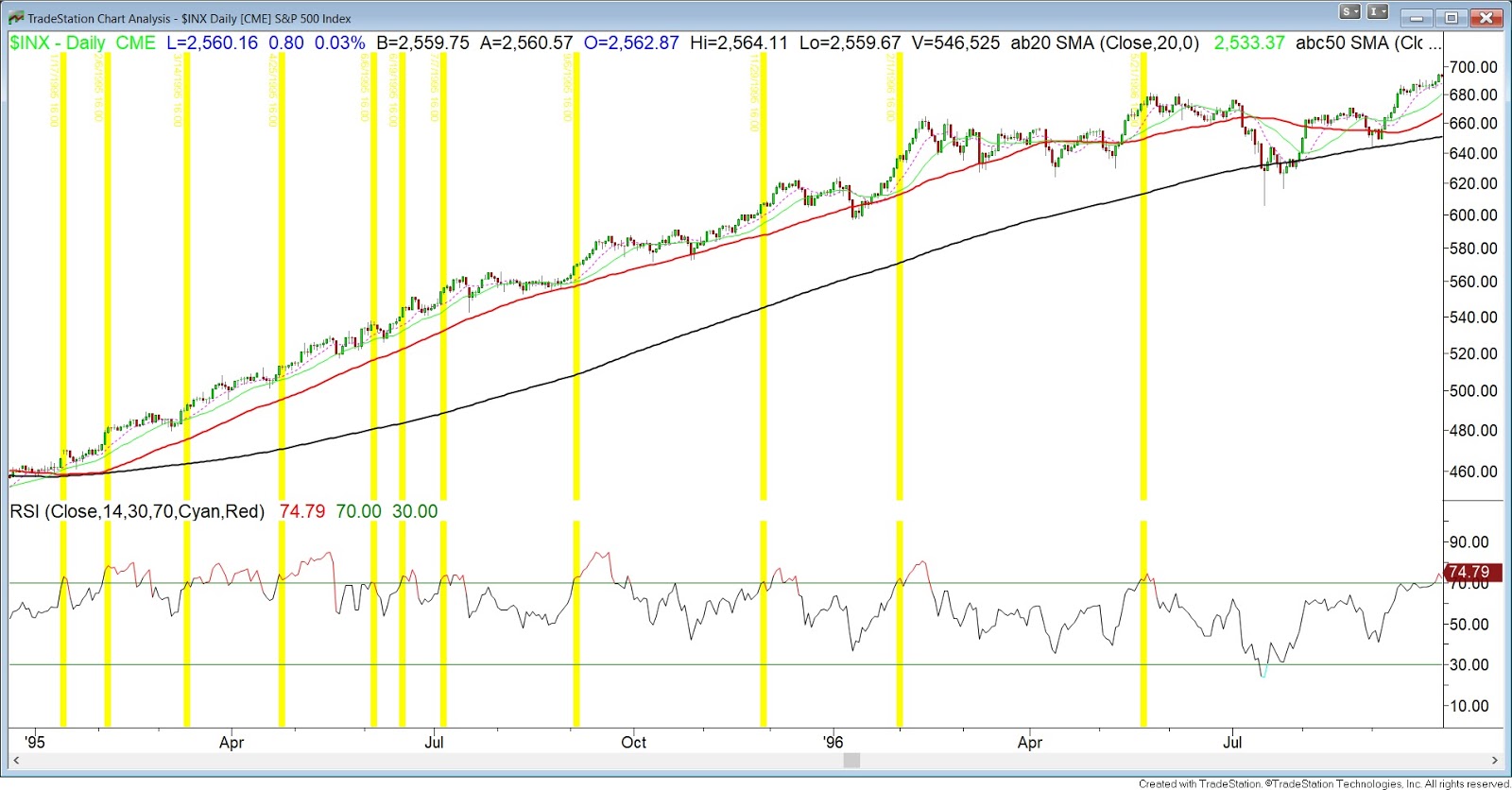

Below is a chart of the S&P with a simple 14 day RSI. We know from historical data that an overbought RSI doesn't necessarily mean we are due for weakness. In some instances it is forecasting future strength and in other cases it anticipates potential pitfalls. The data going back to 1960 shows no statistical edge going out a few weeks or months trying to predict an overbought RSI. In previous posts we have referred to prior strong trending years for comparison purposes. We still believe these to be true and why we are highlighting this below. 1995 was one of the strongest trending years in recent past and we can see that the RSI stayed overbought for much of the year while the S&P trended higher. The 2013-14 market had multiple instances of an overbought RSI all the while the market trended higher for months. This year is shaping up much in the same fashion as these two years. What we have noticed is that in most cases when the 14-day RSI became overbought the S&P went on to consolidate or pullback in the near future. As with any indicator it is not full proof but it is something that we watch and heightened our risk metrics.

Next we wonder if the S&P has broken out to the upside from its 12 month ascending wedge pattern. The path of least resistance is higher and if we do get a pullback we'll be watching the top of that channel for support. What we don't want to see is a hard sell off back into the range causing a failed upside breakout. This could lead to a longer consolidation.

Another useful tool is the monthly fund manager survey (FMS) from BAML. It always offers an interesting view on the global investing landscape and is a good barometer of current market sentiment. Below are the key takeaways that we focused on.

One data point that backs up the case for a potential pullback is that global equity overweight suggests risks ahead for stocks. With global equity net overweight now at +45% this has historically coincided with equity underperformance versus bonds & cash over the next 3 months.

Fund managers are positioning themselves for higher rates as just 3% of investors think global bonds will be lower in the next 12 months. 82% say bond yields will rise and a record 85% say bonds are overvalued. The rotation into banks (biggest in 3 years) and Japan while selling utilities, emerging markets, healthcare, and bonds is evidence managers expect higher yields ahead.

Cash has fallen to 4.7% but still remains high as this is a catalyst for shallow pullbacks. Managers are waiting for any dip to put cash to work.

Through all of our research we continue to conclude the general markets remain in a secular bull market. One of our thesis was the strong backdrop of our economy coupled with growth in earnings is what is propelling equity markets higher. Below supports our opinion as the expectation for macro "Goldilocks" (above-trend growth, below-trend inflation) is at record highs. It is the first time since March 2011 this exceeds investor belief in below-trend growth & inflation as the driver of financial markets.

In summary with the current overbought conditions along with global equity overweight we are mindful for a potential pullback/consolidation at any moment. Yet with cash levels still high to support dip buyers and a stable and growing economy the bull market is alive and well. To strengthen the bull case we are entering a seasonably strong period in the market that we discussed in our last blog. With earnings season upon us, we'll be looking to put cash to work in fresh new ideas but not chasing strength blindly considering the current outlook.