As was probably anticipated, the holiday-shortened week was rather boring and quiet which is likely what allowed the S&P 500 to drift higher by 2.7%.

When the index closed at mid-day on Thursday it had just barely stepped into positive territory for the year and now sits up 0.1%.

The rally in stocks was fueled in large part by energy-related names as the price of oil jumped 10% over the course of the week. This helped the XLE lead all S&P sector ETFs this week in what was virtually across-the-board strong performance.

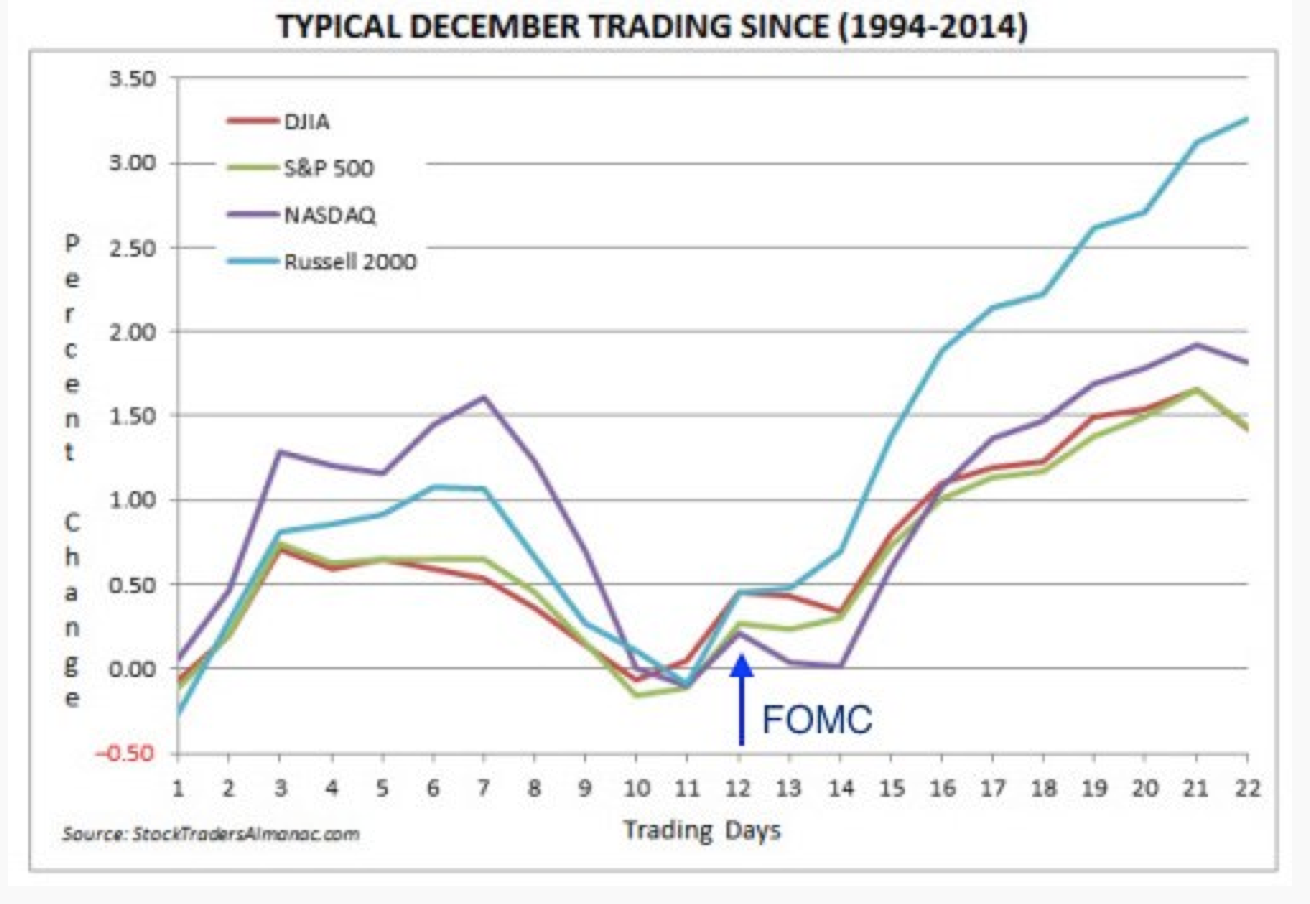

We're likely in store for a similarly quiet environment next week as there are just 4 trading days and Thursday marks the final day of 2015. While December has historically been a very bullish month for the market, people often associate the notion of the Santa Rally with the entire month. However, Ryan Detrick's work and the work of others, has gone to show that the "true" Santa Rally (if there is such a thing) typically starts on December 24th and carries through the 2nd trading day of the following January.

Detrick did a ton of other work on this topic and December seasonality in general. Find that here.

Have a great week and a wonderful new years. We'll see you in 2016.