- Last 20 years: February ranks eighth in monthly performance with an average loss of 0.02%

- Last 20 years: The average daily trend is choppy and trend-less

- Last 20 years: February is the forth most volatile month

- Since 1950: February ranks ninth in monthly performance with an average gain of 0.10%

- Since 1950: February is the 9th most volatile month and is higher 56% of the time

- Since 1950: January is tied with July with the most 5% or greater monthly gains

We want to see what the S&P did for February, full year, and the rest of the year after gaining more than 5% in January. The sample size is small with only 12 prior instances going back to 1950 but still paints a rosy picture for 2018. We took it a step further in the second study looking for prior instances of a 5% or greater January and the prior month hit a new high Even smaller sample size but still remains bullish.

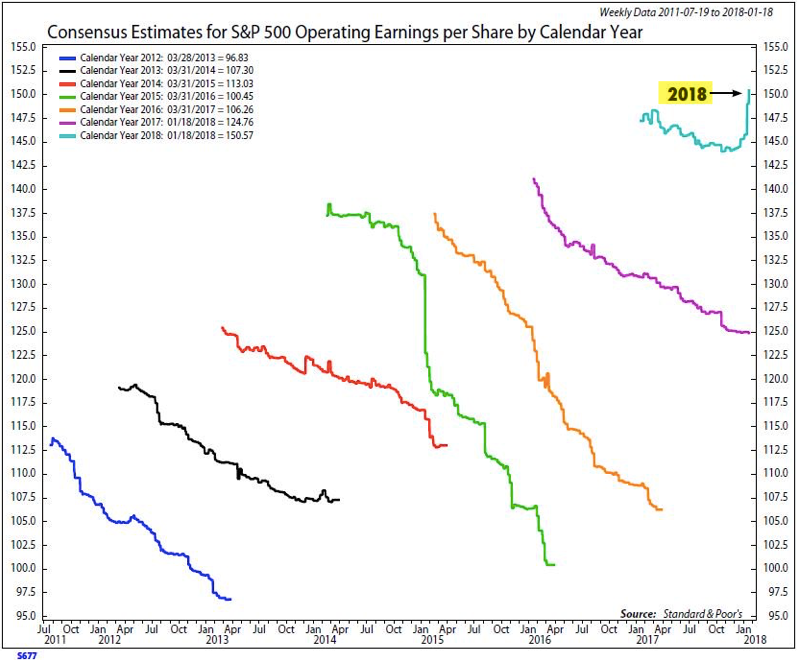

One of the main reasons driving this bull market is that we are going from a QE market to an earnings driven market. This is the first time in a while that earnings revisions are actually be raised rather then revised downward throughout the year (from NDR).

There is a legitimate concern about the rise in rates and rightfully so. However, we looked at the data when the S&P was up more than 5% and the TNX (10 yr yields) are up greater than 10% just like this January and we find that the returns in the S&P remain favorable to the bulls going out 1,2,3, and 6 months. Are the rise in rates signaling a better economy? We think so, and also believe that rates will have to be much higher before they become a big problem. There was only one prior instance of January gaining more than 5% and TNX gaining more than 10%. That was in January 2013.

The 3 major averages all broke their steep up trend-line from the January lows on Tuesday. This simple 1% down day, which was the first one in 112 days, caused traders to panic and it seems as if sentiment went from overly optimistic to extremely bearish in one day. The CNN fear and greed index sits at 61 as it pulls back from extreme greed at the same time the put call ratio spiked along with the VIX. Yet, the S&P broke the record for number of days without a 5% correction this month. The US equity markets have started the year off on a hot start. We don't expect the same bullishness every month this year but the stats favor another strong year. Even though we remain bullish longer term we expect bouts of volatility to increase throughout the year and having a tactical view will prove to be prudent.