Elsewhere, investors betting on the Russell 2000 to show some outperformance were finally rewarded with a strong month as the small cap index rose 3.12%. And, as has been the theme for the year, the Nasdaq logged more gains with a 1.09% move higher.

On a sector basis (using S&P sector ETFs), the market was pulled higher primarily by Financials. And in a welcome change, Energy (XLE), even though it pulled back from its monthly highs, was able to finish flat for November and hang onto the impressive October gains.

The Nasdaq's November gains now leave it up nearly 8% year to date and well ahead of the other primary domestic equity benchmarks. Also of note, the Russell 2000 and Dow Jones Industrial Average are both near flat for the year after having spent much of 2015 solidly in the red.

The year-to-date returns shown above have left most investors feeling little more than uninspired and the study below by Bespoke digs a little deeper to show why stock market returns have been so "blah" this year. They looked at the Russell 3000 and found that the largest 1% of companies in the index are up an average of 6.6% while the other 99% of stocks are down an average of -3.2%. That's pretty amazing...and depressing. We've said it throughout the year that market leadership has been incredibly narrow and this picture drives the point home further.

Barring a last minute change of direction and/or deterioration of the data (see: today's ISM report), the Federal Reserve looks set to raise its target interest rate by 25bps later this month and the market seems to have come to accept this as fact. Assuming the Fed does not surprise with any concerning commentary, the stage could be set for yet another year end "Santa Rally."

There's no shortage of data available to suggest that the "Santa Rally" or whatever you want to call it is in fact a real phenomena. Here's a couple samples:

|

| -Jeff Saut (Raymond James) |

And according to one of our favorite market observers, Ryan Detrick, if the market finishes strong today, history says we could really be setting up for a decent December. Since 1950, when the S&P has been up on the first trading day of December (which it has 32 times), it has gone on to average a return of 3.37% for the month with 30/32 instances finishing with positive returns (a 94% win rate).

We always caution against relying too heavily on seasonality but some of these stats really are compelling and point to some consistent forces that appear to want to push the market higher in December.

Going back to the Fed's likely decision to raise rates, one would figure that it would strengthen the US dollar even further as other economies continue to ease. If in fact the dollar does proceed upward, that will likely continue to have a negative impact on the commodities complex (we touched on this last week re: oil) and economies that are heavily commodity-based. The chart below from 361 Capital would agree and suggests that such a scenario favors US stocks as the equity market of favor relative to the rest of the world.

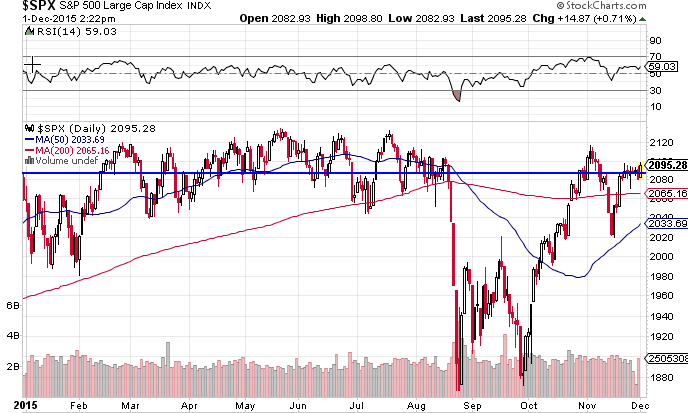

Barring a thrilling December move (in either direction), 2015 looks set to go down as a year where the market went "nowhere." We see below that even with the late August - September plunge, we've really just fluctuated around this area for basically a full year now.

However, going back to our friend Mr. Detrick, he pulled a stat that's pretty encouraging if we do indeed finish out the year relatively "flat." He found that S&P returns after a "flat" year (which he defined as a calendar year return between -3% and +3%) have been incredibly strong. There have been 7 years since 1960 where the S&P met his definition of "flat." The index has averaged a return of 19% in the years following and has never returned less than 10%. After the year most investors have had, we're pretty sure they'd be ok with that type of outcome in 2016.