In our role of portfolio management we always want to play devils advocate and poke holes in our thesis so we don't turn a blind eye to potential pitfalls. The data above certainly paints a bullish picture the next few months. In our last blog on divergences we highlighted how momentum has peaked creating a negative divergence. Below we look at the recent weakness in high yield and what that may forecast for the equity markets. We can see in 2017 when high yield index has broken down this leads to a slow down in equity markets. Is this time different? We don't have the answer to that but it is something we continue to monitor.

If we turn our attention to the monthly fund manager survey (FMS) from BAML, there are a some levels that are flashing a more cautious tone. Below is a recap of the current month takeaways straight from the November report.

- It’s frothy FAANG: big market conviction in Goldilocks (+ price action in FAANG/BAT,

Bitcoin) leading to bull capitulation; FMS risk-taking hits all time high (Exhibit 1), cash

decisively lower despite record high saying equities overvalued (= irrational

exuberance)…our conviction in winter post-tax reform risk asset correction hardens - Consensilocks: all-time high Goldilocks expectations (56% expect “high growth, low

inflation”); contrasts with tumbling bear view of secular stagnation as macro backdrop

(was 88% Feb’16, now 25%); US tax reform expected to sustain or inflate Goldilocks - Ever closer to the sun: Nov FMS cash level drops to 4.4% from 4.7% = lowest since

Oct’13 & no longer a “buy signal”; FMS hedge fund equity exposure at 11-year high;

BofAML Bull & Bear Indicator up to 7.2 but sell-signal not yet triggered - Correction catalysts = inflation & market structure: biggest FMS risk to EPS =

wage inflation; rising FMS concerns re “market structure” (3rd biggest tail risk);

strategies most likely to exacerbate correction…vol selling (32%), ETFs (28%), risk parity

(16%) - Notable FMS takeaways: crowded trades are #1 long Nasdaq, #2 short volatility, #3

long credit; highest global equity OW since Apr’15, highest Japan OW in 2-years, an epic

FMS UW in UK assets, and big Nov rotation to energy from bank stocks - Contrarian stagflation trades: long UK, short Eurozone; long pharma, short banks;

long utilities, short tech

The S&P’s split personality. Last week, there were a lot of buying climaxes (reversals from 52-week highs) in S&P 500 stocks - 32 of them, which was up from 20 the prior week. There were also a lot of selling climaxes (reversals from 52-week lows), 17 of them, which is highly unusual in a week when there were so many buying climaxes. Usually there are many of one or the other, not both. The only time we’ve seen so many of both kinds of reversals, showing a highly split market, was in March 2000.

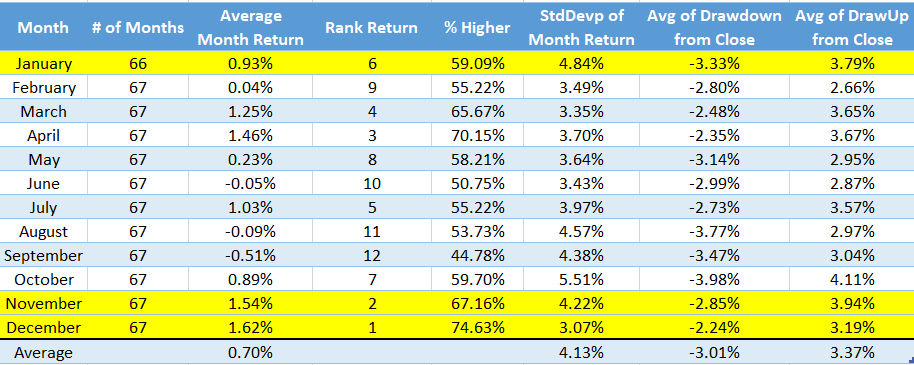

Once again we have presented alternative view points for both bulls and bears to consume. We remain firmly in the bullish camp as we continue to operate within our secular bull market assumption. However with some negative divergences appearing along with some inflated conditions to the upside we have some cash on the sidelines to put to work on any weakness as we look for a strong close to year end.

We hope everyone has a safe and wonderful Thanksgiving! We certainly are thankful over at Worch Capital for all blessings we have.