The markets are rallying hard into year end on the backs of promising vaccine news coming out of multiple pharmaceutical companies and the election out of the way. This is great news for the country and the world. The quicker we can get past COVID the better off we all are. As of this moment, the Russell 2000 is up 16% in November while the S&P 500 is up close to 11%. The energy sector is up a whopping 25%. The vaccine news has caused a huge rotation into beaten down sectors as the play on the economy opening back up has been strong. Meanwhile, traditional COVID stocks have been beaten up in a giant rotation trade. While we believe the markets will finish the year strong, the renewed optimism in growth may have gotten a little ahead of itself as the markets are now overbought in the short term.

The recent BAML fund manager survey gives us a good indication on sentiment and positioning of fund managers. Below are the key takeaways from the November report that shows a shift to a bullish crowd:

Bottom line: the most bullish Fund Manager Survey (FMS) of 2020 on the back of vaccine, election, macro; Nov FMS shows a big drop in cash, 20-year high in GDP expectations, big jump in equity, small cap & EM exposure; reopening rotation can continue in Q4 but we say "sell the vaccine" in coming weeks/months as we think we're close to "full bull".

Cash bears: FMS cash levels sink to 4.1% from 4.4%, now below the pre-COVID-19 level (was 4.2% in Jan), close to triggering FMS Cash Rule "sell signal" (occurs when cash <4% - see Rules & Tools); BofA Bull & Bear Indicator trending higher at 4.2.

Vaccine bulls: COVID-19 remains #1 "tail risk"; but FMS investors continue to pull forward their timing of "credible vaccine", now expected Jan'21 (was Feb'21).

Macro bulls: global growth & profit optimism at 20-year high; big majority (66%) now say macro in "early-cycle" phase, not recession; small majority of CIOs still want CEOs to improve balance sheet (47%), but desire for capex (the 2021 key to sustained economic recovery) on the rise (38%).

Risk bulls: all-time high in FMS investors expecting a steeper yield curve (73%); allocation to equities (net overweight 46%) highest since Jan'18 and close to extreme bullish (i.e. >50%); allocation to cash (net 7%) lowest since Apr'15.

Rotation bulls: Nov FMS shows unambiguous rotation to EM, small cap, value, banks, funded by lower allocation to cash, bonds, staples; note cyclical assets such as EAFE (Japan, Eurozone, UK) and energy stocks lagging the Q4 bullish rotation.

2021 fave trades: asked for their 3 favorite 2021 Year Ahead trades, FMS investors said #1 long Emerging Markets, #2, long S&P500, #3 long oil (Chart 1); FMS investors still regard long tech as by far and away most "crowded trade" in Nov'20.

Nov FMS contrarian trades: Q4 contrarian bulls would position for completion of "full bull" reopening rotation via longs in Japan, Eurozone, UK, and energy stocks; contrarian bears would position for flatter yield curve trades e.g. long staples heading into late-20/early-21 "top".

The bullishness of fund managers is corroborated by other sentiment measures. Below we can see how optimistic fund managers are, as their optimism increases to highest level since January 2018. The recent AAII survey is similar as it shows the bulls have the highest reading since January 2018 to go along with the largest weekly jump since July of 2010. While the CNN fear and greed index is flashing a greedy signal. On top of that US equity inflows had the second largest increase on record.

Clearly sentiment has caught up to the aggressive price moves over the last month. The Russell 2000 is now above its weekly bollinger band and overbought. We can see the rotation as small caps have outperformed drastically. This shows up in fund managers over-weighting small caps over large caps. They also resumed a cyclical rotation into laggards since the election.

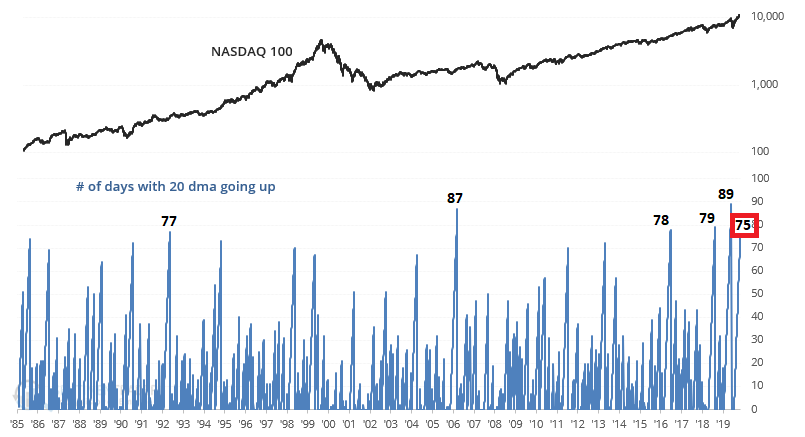

As sentiment has reached excessive levels along with the general market becoming overbought it has created extremely strong breadth readings since the rally off the election lows. The % of stocks trading above their 10, 20, 50, and 200 day moving averages has surged in the past month as the S&P hit new highs.

Ryan Detrick, in a recent tweet, confirms this is bullish looking forward when we see extreme breadth. "Last week saw more than 85% of the components in the S&P 500 above their 200-da MA. This is quite rare and suggests extremely strong breadth and participation. The future 1,3, 6 and 12 months returns are stronger than average when this happens."

Is the market setting up a false sense of bullishness as we enter the flu season and a spike in COVID cases just as market participants turned excited. Or will traders see through the negative COVID headlines and look beyond that as vaccines get administered, the Fed remains cooperative, and the potential for another round of stimulus? We believe the market has gotten ahead of itself in the short term and needs some time to digest the new growth narrative and rotation. However, the trend remains our friend and the path of least resistance remains higher. Until that changes we see no reason to turn bearish and continue to operate under the assumption the markets remain in a secular bull market with months and years left to run.

One of our main concerns we identified in our last post was the excessive move in the indices on weakening breadth. This negative divergence on its own isn't completely bearish. What it needed was a break in price to confirm the signal. The Nasdaq certainly had a break as it had the fastest 10% correction off all-time highs ever while also breaking its trend-line support. The S&P remains in the channel but is testing the lower trend-line.

One of our main concerns we identified in our last post was the excessive move in the indices on weakening breadth. This negative divergence on its own isn't completely bearish. What it needed was a break in price to confirm the signal. The Nasdaq certainly had a break as it had the fastest 10% correction off all-time highs ever while also breaking its trend-line support. The S&P remains in the channel but is testing the lower trend-line.

{kind=link}